This website uses cookies to improve your browsing experience. By continuing to use this website you agree to our use of cookies. For more information on our use of cookies, click here to review the Cookies Policy.。

Taiwan's new anti-avoidance rules on controlled foreign companies (the "CFC Rules") will take effect in 2023, after which the scheme where multinational corporations keep the earnings of their portfolio companies in a low-tax country or region overseas and do not repatriate them to Taiwan to defer taxation will no longer be effective. Pursuant to Article 43-3(1) of the Income Tax Act, except under certain exemptions, corporations and their affiliates who directly or indirectly hold 50% or more of the shares or capital of an affiliate in a low-tax country or region outside of Taiwan or have significant influence over such affiliate should recognize the investment proceeds from the earnings of such affiliates in the current year based on the percentage of shares or capital they held in such affiliate and the period of the ownership, and include such investment proceeds in its current year's taxable income.

The Ministry of Finance (the "MOF") has announced that the Taiwan CFC Rules and the "Regulations Governing Application of Accrued Income from Controlled Foreign Company for Profit-Seeking Enterprise" (the "Profit-seeking Enterprise CFC Regulations" or the "Regulations") will take effect in 2023. Furthermore, the MOF provides certain examples for the income recognition and calculation under the Regulations (see below). This article is a brief introduction for your reference.

Criteria of Exemption

To adhere to the spirit of the CFC Rules and to consider the burden on both the tax authority and the tax payer, the CFC Rules may exempted when either of the following conditions is satisfied:

1.where the CFC at issue has substantial business activities in the country or region where it is located; or

2.where the annual surplus of the CFC at issue, on an individual basis, is less than NT$7 million. However, where the total surplus or deficit for the year of all the CFCs of the tax payer at issue is a positive figure and exceeds NT$7 million, the earnings for the year of each such individual CFC should be included in the tax payer's taxable income of the current year.

Calculation of CFC's Current Year Earnings

What constitutes a CFC's current year earnings and which part of its investment proceeds should be included in its parent corporation's taxable income? First, the calculation of a CFC's current year earnings is based on its current year's net income after tax calculated under Taiwan's GAAP. However, considering that its portfolio company located in a non-low-tax country or region may need to retain earnings as working capital or to meet its investment needs and not for tax avoidance purposes, its investment proceeds from portfolio companies in non-low-tax countries or regions recognized under the equity method are recognized as the CFC's current year earnings based on the actual distribution (realized loss), and the calculation formula is as follow:

CFC's current year earnings = the amount of its current year's after-tax net income, other comprehensive income or loss, and other equity items recognized as the current year's undistributed earnings, as calculated in accordance with Taiwan GAAP, plus items 1 and 2 and minus items 3 to 4 below:

1.(the approved distribution from its portfolio company's earnings in countries or regions other than the People's Republic of China (the "PRC") recognized under the equity method – income tax on the dividends or earnings paid in those countries or regions) x the percentage of the CFC's ownership of the portfolio company at the date of the distribution

2.distribution of the portfolio company's earnings in the PRC recognized under the equity method x the percentage of the CFC's ownership of the portfolio company at the date of the distribution

3.the portfolio company's investment proceeds in non-low-tax countries or regions recognized under the equity method– the portfolio company's investment loss in non-low-tax countries or regions recognized under the equity method

4.the portfolio company's realized investment loss in non-low-tax countries or regions recognized under the equity method × the percentage of the CFC's holdings in the portfolio company at the date of the realization

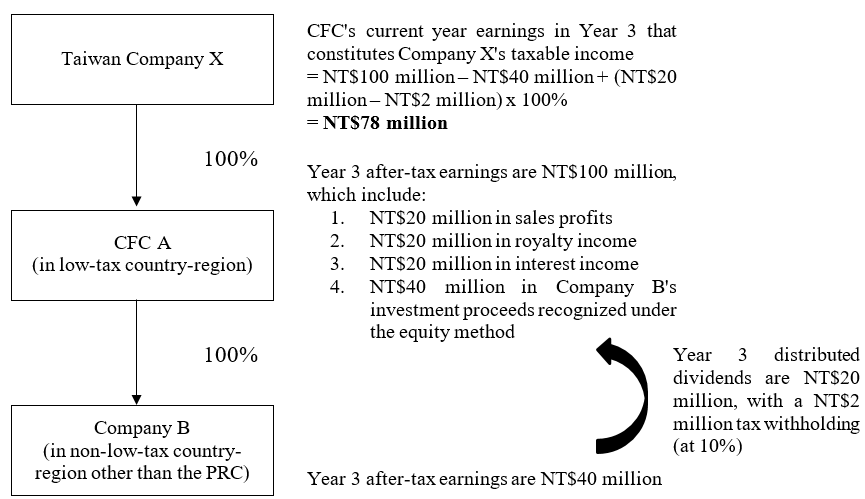

For instance, Taiwan Company X owns 100% of Company A (a CFC of Taiwan Company X located in a low-tax country) and Company A owns 100% of Company B (located in a non-low-tax country/region other than the PRC). Company A's after-tax earnings for the year as shown on its financial statements prepared in accordance with Taiwan GAAP (the "after-tax earnings") for the year is N$$100 million (including NT$20 million of sales profit, NT$20 million of royalty income, NT$20 million of interest income, and NT$40 million of investment proceeds from its portfolio companies recognized under the equity method), and Company B's board of directors decided to distribute NT$20 million of dividends, which is subject to a withholding tax rate of 10%. Company A does not meet the exemption criteria of the CFC Rules. Question: What is CFC A's current year earnings?

CFC A's current year earnings = Company A's after-tax earnings – Company B's investment proceeds recognized under the equity method + (Company B's approved dividend distribution - dividend withholding tax paid in Country B) × Taiwan Company A's shareholding percentage in CFC A

= NT$100 million - NT $40 million + (NT $20 million - NT $2 million) × 100%

= NT $78 million

Calculation of Investment Proceeds that Constitute Taxable Income

After determining that CFC A's earnings of the year is NT$78 million, how much of it should be included in Taiwan Company X's taxable income? According to Article 6(1) and (2) of the Regulations, corporations should calculate their CFCs' earnings of the current year in accordance with Article 5(5) of the Regulations. That is, a corporation should withhold any legal reserve and non-distributable amount in accordance with the laws of the countries or regions in which the CFCs are located and any prior years' losses as assessed by the taxing authority, before including such investment proceeds into its taxable income for the current year based on its direct ownership of the CFCs' shares or capital and the period during which it holds such shares or capital. The calculation formula is as follows:

CFC's investment proceeds that should be included in its parent corporations' taxable income = (CFC's current year earnings - legal reserve or non-distributable amount specified under the laws of the country or region where the CFC is located - prior years' assessed losses for each period) × direct holding percentage × holding period

The "prior years' assessed losses for each period ", as referred to in the above formula, should be subject to the following rules:

1.The losses should be assessed by the local tax authority in the jurisdiction where the parent corporation is located, based on the CPA-certified financial statements or other supporting documents prepared pursuant to the instructions of the parent corporation (which should recognized and report the CFC's loss for each period in accordance with the laws), from the year in which an affiliate constitutes a CFC, before the parent corporation is allowed to deduct the losses of the CFC from the earnings of the CFC for 10 years from the year following the year in which the losses occurred;

2.Where a CFC's current year earnings do not reach NT$7 million, its assessed losses for prior years should still be deducted from the CFC's current year earnings; and

3.When the CFC applies for a capital reduction to cover losses, the amount of the capital reduction should be deducted from its assessed losses for prior years.

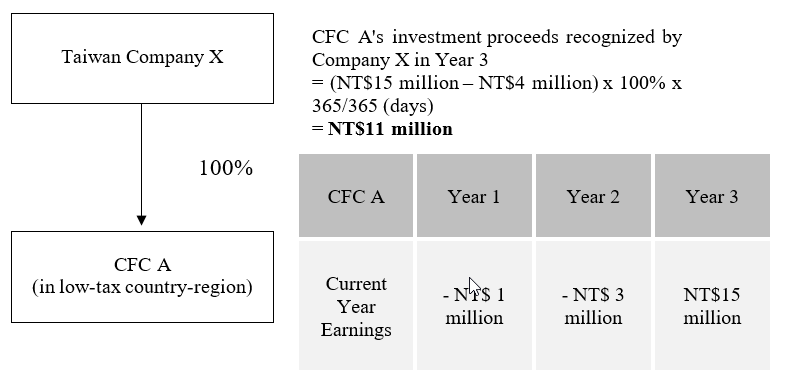

For instance, Taiwan Company X has held 100% of Company A (Taiwan Company X's CFC located in a low-tax country) for three years, and the assessed losses of the CFC in the first and second years were NT$1 million and NT$3 million, respectively, and the CFC's earnings for the third year is NT$15 million. In calculating the third year's taxable income, Taiwan Company X should use the CFC's current year earnings of NT$15 million and deduct the assess losses of NT$1 million and NT$3 million, respectively, from the CFC's current year earnings, and then recognize the investment proceeds of NT$11 million based on its shareholding percentage of 100% and include it in its current year's taxable income.

Calculation for Avoiding Double Taxation

After a corporation includes the investment proceeds of its CFCs into its taxable income for the current year, in order to avoid double taxation when dividends or earnings are actually distributed by the CFCs subsequently, in accordance with Article 7(1) of the Regulations, when a corporation actually receives the dividends or earnings of its CFCs, the portion of the investment proceeds already recognized and included in its taxable income should be excluded from the current year's taxable income, while the remaining portion should be included in its taxable income of the current year.

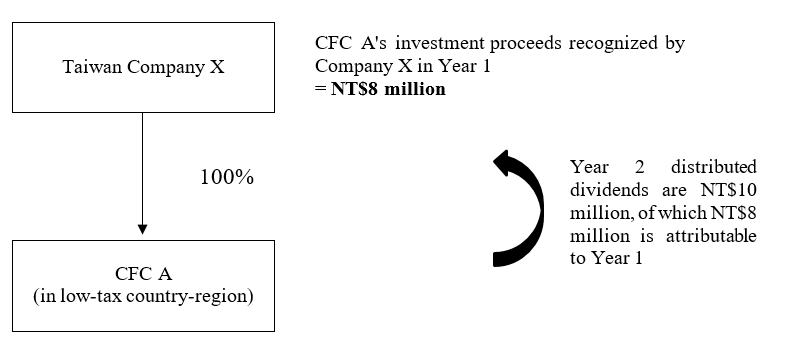

For instance, Taiwan Company X owns 100% of Company A (Taiwan Company X's CFC located in a low-tax country). In Year 1, pursuant to Article 43(3) of the Income Tax Act, Taiwan Company X includes the investment proceeds (which come to a total of NT$8 million) from Company A's CFC into its taxable income. In Year 2, Company A distributed of NT$10 million of dividends (of which NT$8 million was earnings in Year 1), and Taiwan Company X was distributed NT$10 million of the dividends, of which NT$8 million was already recognized as CFC investment proceeds for tax purposes in Year 1 and therefore was not repeatedly included in the taxable income in the year of the distribution (i.e., Year 2). The remaining NT$2 million should be included in the taxable income in the year of the distribution (i.e., Year 2).

Tax Refunds and Deductions

Article 7(2) of the Regulations stipulates that the income tax paid by a corporation on the dividends or earnings from its CFCs pursuant to the local income tax laws thereof is deductible from the tax payable in the year in which the investment proceeds are recognized within five years from the day after the expiration of the filing period for the year in which the investment proceeds are recognized, and any excess tax paid may be refunded. Where the distributed dividends or earnings are from the investment proceeds of a PRC portfolio company, the dividends or earnings income tax paid in the PRC and the corporate income tax and dividend or earnings income tax paid in a third jurisdiction may be deducted from the amount of tax payable in the year in which the investment proceeds are recognized within the period prescribed above, and any excess tax paid may be refunded. The amount of the deduction should not exceed the increase in taxable amount calculated at the applicable domestic tax rate as a result of the addition of the investment proceeds.

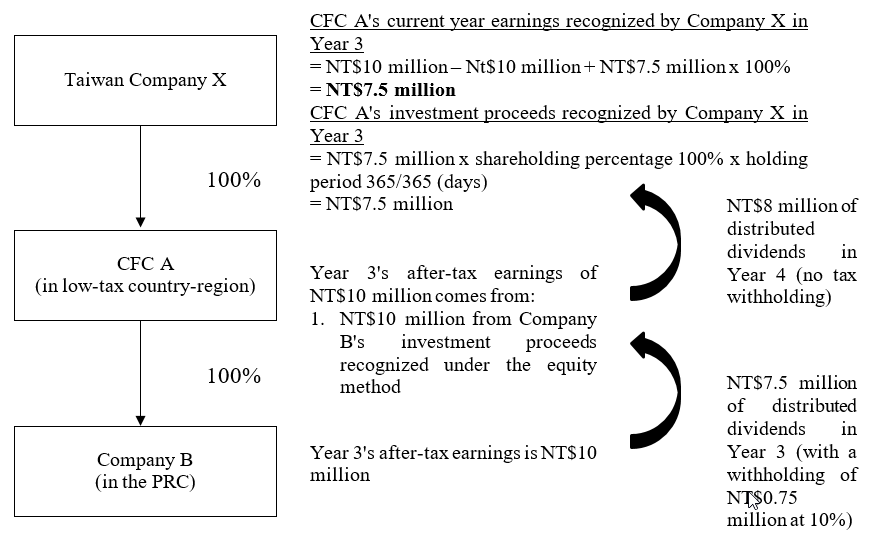

For instance, Taiwan Company X owns 100% of Company A (a CFC of Taiwan Company X located in a low-tax country) and Company A owns 100% of Company B (which located in the PRC). In Year 3, Company B had an after-tax earnings of NT$10 million, distributed NT$7.5 million of dividends during the year, and paid NT$750,000 of dividends income tax in the PRC (at the withholding rate of 10%). In the same year, Company A recognized only NT$10 million of Company B's investment proceeds as its after-tax earnings; Taiwan Company X had a domestic income loss of NT$5 million, NT$9 million of income from the PRC (exclusive of its CFCs' investment proceeds), and had paid NT$900,000 in the PRC. Question: What is the amount of tax payable by Taiwan Company X for Year 3?

1.Current Year Earnings of Company A (i.e., the CFC)

= CFC's net income for the year calculated under Taiwan GAAP - investment proceeds from portfolio companies in non-low-tax countries or regions recognized under the equity method+ (approved distribution from earnings of portfolio companies in the PRC recognized under the equity method x the percentage of the CFC's holdings in the portfolio companies at the date of the distribution)

= NT$10 million - NT$10 million + (NT$7.5 million × 100%) = $7.5 million

2.Investment proceeds that should be recognized by Taiwan Company X in the current year pursuant to the CFC Rules

= CFC's current year earnings × direct holding ratio × holding period

= NT$7.5 million × 100% × 365 ÷ 365 days = NT$7.5 million

3.Calculation of deductible amount

i.Maximum tax credit for income generated in the PRC (including CFC's investment proceeds)

= the tax payable by Taiwan Company X calculated based on its total taxable income at the applicable domestic tax rate - the tax payable by Taiwan Company X calculated based on its income generated in Taiwan at the applicable domestic tax rate

= (- NT$5 million + NT$9 million + NT$7.5 million) × 20% - NT$0 = NT$2.3 million

ii.Local tax paid on income generated in the PRC = NT$900,000

iii.Since the maximum amount of tax credit for income generated in the PRC is NT$2.3 million, which is higher than the NT$900,000 of local tax paid on income generated in the PRC, the amount of tax credit available is NT$900,000.

4.Calculation of Tax Payable

= the tax payable by Taiwan Company X calculated based on its total taxable income at the applicable domestic tax rate- deductible amount

= NT$2.3 million - NT$0.9 million = NT$1.4 million

Taiwan Company X's tax payable in Year 3 is NT$1.4 million. If the CFC A's board of directors decided to distribute dividends in Year 4, how should Taiwan Company X calculate the refundable tax amount for Year 3 after corresponding adjustment?

Assuming Company B's after-tax earnings in Year 4 is NT$0 and Company A's after-tax earnings in Year 4 is also NT$0, Company A's board decided to distribute NT$8 million of dividends (which is subject to a 0% withholding rate) during the year, Taiwan Company X declared that out of the NT$8 million in dividends from Company A, NT$7.5 million was already recognized as its CFC's investment proceeds in Year 3, and should not be counted again in Year 4 as a part of its taxable income. As the proceeds were generated in the PRC, the NT$750,000 of dividends income tax paid is subject to correction and recalculation of the tax credit for Year 3 under the tax laws of the foreign country where the income was generated. The remaining dividends income of NT$0.5 million should be included in the taxable income in the year of distribution (i.e., Year 4), and the PRC dividends income tax of NT$50,000 should be offset against the taxable amount of the year of distribution.

1.Maximum tax credit for income generated in the PRC (including CFC's investment proceeds)

= the tax payable by Taiwan Company X calculated based on its total taxable income at the applicable domestic tax rate - the tax payable by Taiwan Company X calculated based on its income generated in Taiwan at the applicable domestic tax rate

= (-NT$5 million + NT$9 million + NT$7.5 million) × 20% - NT$0 = NT$2.3 million

2.Local tax paid on income generated in the PRC = NT$900,000 + NT$750,000 = NT$1.65 million

3.Since the maximum amount of tax credit for income generated in the PRC is NT$2.3 million, which is higher than the NT$1.65 million of local tax paid the income generated in the PRC, the amount of tax credit available = NT$1.65 million

4.Taiwan Company X's tax refunds for Year 3 after adjustment

= the tax payable by Taiwan Company X calculated based on its total taxable income at the applicable domestic tax rate- deductible amount - self-assessed amount paid

= NT$2.3 million - NT$1.65 million - NT$1.4 million = - NT$750,000

Sale of CFC Shares or Capital

Finally, when a corporation sells its CFC shares or capital, how should the sales profit or loss calculated in accordance with the CFC Rules?

In accordance with Article 7(3) of the Regulations, when corporations dispose of CFC shares or capital, the gain or loss on disposal is calculated in accordance with the following provisions.

1.Disposal gain or loss = Disposal income - original acquisition cost - (the balance of the investment proceeds recognized on the disposal date of the CFC × disposal percentage)

2.The balance of the investment proceeds recognized on the disposal date of the CFC

= Accumulated CFC investment proceeds recognized in accordance with the CFC Rules up to the date of disposal - the actual dividends or earnings distributed in prior years that were not included in the income in the year of distribution in accordance with the CFC Rules - the amount deducted from the balance of the CFC's investment proceeds based on the disposal percentage in prior years.

For instance, Taiwan Company X purchased five hundred shares of Company A for NT$100 million and acquired 100% of Company A (Taiwan Company X's CFC). In Year 1, Company A had an after-tax earnings of NT$10 million and Taiwan Company X recognized NT$10 million of investment proceeds from CFC in its financial statements for Year 1. On June 1 of Year 2, Company A distributed NT$8 million of dividends, of which $6 million was already recognized as investment proceeds in Year 1, and was not included in the taxable income of the year in which it was distributed (i.e., Year 2), while the remaining NT$2 million of dividends should be included into the taxable income in the year it was distributed (i.e., Year 2). In Year 2, Company A had an after-tax earnings of NT$10 million and Taiwan Company X recognized NT$10 million of investment proceeds from CFC in its financial statements for Year 2. On January 1, Year 3, Taiwan Company X sold fifty shares of Company A (which accounts for 10% of Company X's shareholding percentage that day) for NT$4,000,000 (the remaining 450 shares represent 90% of Company A's equity). In Year 3, Company A had an after-tax earnings of NT$10 million and Taiwan Company X recognized NT$9 million of investment proceeds from CFC in its financial statements for Year 3. Question: What is the amount of the gain or loss on the sale of Taiwan Company X's shares?

Calculation of gain or loss on sale of shares of Taiwan Company X in Year 3:

1.The balance of the investment proceeds recognized on the disposal date of the CFC

= CFC investment proceeds recognized in Year 1 - dividend received in Year 2 but excluded from income tax in the year of distribution + CFC investment proceeds recognized in Year 2

= NT$10 million - NT$6 million + NT$10 million = NT$14 million

2.Original acquisition cost = Original cost × Disposal percentage

= NT$100 million × 10% = NT$10 million

3.Disposal gain or loss = Disposal income - original acquisition cost - (the balance of the investment proceeds recognized on the disposal date of the CFC × disposal percentage)

= NT$40 million - NT$10 million - (NT$14 million x 10%)

= NT$28.6 million

Conclusion

Taiwan CFC rules and the Regulations will have a substantial impact and become a big challenge to the long-standing thinking and practice of corporations utilizing foreign companies in their business groups. This is the time to gain in-depth understanding on the tax issues and risks that may arise after the implementation of the CFC Rules, and plan appropriate countermeasures, such as adjustments to the investment scheme and shareholding structure, changes to the transaction process and order taking models. In addition, when family enterprises face the CFC issues, they should pay close attention to the disclosure of foreign investment structure and financial statements of foreign companies, and whether it will lead to the taxation of past overseas income or even estate and gift tax. The best way to resolve any concerns in this regard is to make use of the six-month precious window before the implementation of the CFC Rules and consult with professionals to obtain the necessary assistance and advice. Our tax team is composed of tax lawyers and certified public accountants licensed in Taiwan and overseas who are familiar with the latest changes in domestic and international tax laws, and we work closely with L&L, Leaven & Co., CPAs and have an in-depth knowledge of taxation practices in Taiwan. If you have any questions about the CFC Rules, please do not hesitate to contact our Tax Practice Group.