Newsletter

The Determination of Related Parties of the Profit-Seeking Enterprises under the CFC Rules

In order to contain the deferred taxation resulting from profit-seeking enterprises’ parking the earnings of invested companies in a low-tax burden country or jurisdiction, Taiwan promulgated Article 43-3 of the Income Tax Act (ITA) on July 27, 2016 to introduce the Controlled Foreign Company (CFC) Rules for profit-seeking enterprises. The Executive Yuan announced on January 14, 2022 that this Article will come into effect in 2023. Meanwhile, in order to define the scope and application of the CFC Rules, the Ministry of Finance (MOF) issued the “Regulations Governing Application of Accrued Income from Controlled Foreign Company for Profit-Seeking Enterprise” (CFC Regulations for Profit-seeking Enterprises) on September 22, 2017, which not only defines the terms of controlled foreign companies, related parties and low-tax burden countries or jurisdictions, but also stipulates the exemption criteria, the calculation of investment income, the treatment of avoidance of double taxation, and the information to be disclosed as well as the documents to be submitted in the declaration, and other implementation details. The effective date of the CFC Regulations for Profit-Seeking Enterprises has yet to be announced by the MOF.

Pursuant to Paragraph 1, Article 43-3 of the ITA, except for those who are eligible for the exemption, any profit-seeking enterprise and its “related parties” directly or indirectly holding 50% or more shares or capital of a foreign affiliated enterprise registered in a low-tax burden country or jurisdiction, or having a significant influence on such foreign-affiliated enterprise, shall recognize the earnings of the foreign-affiliated enterprise as the profit-seeking enterprise’s investment income, which is calculated according to the holding percentage and period of the shares or capital, and such investment income shall be included in the taxable income of the current year. Therefore, when determining whether the CFC Rules apply, in addition to the direct or indirect shareholdings of the profit-seeking enterprise itself, the direct or indirect shareholdings of its “related parties” should also be included in the calculation. Such rule may prevent profit-seeking enterprises from improperly using “related parties” to hold shares or capital of a foreign-affiliated enterprise registered in a low-tax burden country or jurisdiction to avoid the application of the CFC Rules. Apparently, the definition and scope of related parties will have a significant impact on the scope of investment income that should be recognized by the profit-seeking enterprises.

Article 3 of CFC Regulations for Profit-Seeking Enterprises expressly stipulates that “related parties” include any other profit-seeking enterprises related to a profit-seeking enterprise (i.e., “affiliated enterprises”) and any domestic or foreign individuals, institutions or organizations related to a profit-seeking enterprise (i.e., “related parties other than the affiliated enterprises”). Paragraphs 2 and 3 of this Article stipulate, respectively, the criteria of “affiliated enterprises” and “related parties other than the affiliated enterprises” as follows:

“Affiliated enterprises” shall refer to where any of the following relationships exist between a profit-seeking enterprise and another domestic or foreign profit-seeking enterprise:

- A profit-seeking enterprise directly or indirectly holds 20% or more of the total outstanding voting shares or capital stock in another profit-seeking enterprise.

- 20% or more of the total outstanding voting shares or capital stock in two or more profit-seeking enterprise are directly or indirectly owned or controlled by the same person.

- A profit-seeking enterprise holds the highest percentage of the total outstanding voting shares or capital stock in another profit-seeking enterprise and such percentage reaches 10% or more.

- Half or more of the executive shareholders or directors of a profit-seeking enterprise and those of another enterprise are the same.

- The aggregate number of directors appointed by one profit-seeking enterprise and other profit-seeking enterprises in which it directly or indirectly holds over 50% of the total outstanding voting shares or capital stock in another profit-seeking enterprise reaches half or more of the total number of directors of the latter profit-seeking enterprise.

- The chairperson, general manager, or its equivalent or superior of one profit-seeking enterprise is that of another profit-seeking enterprise, or has the relation of a spouse or blood relation within the second degree with that of another profit-seeking enterprise.

- A profit-seeking enterprise directly or indirectly controls the personnel, finance, or business operation of another profit-seeking enterprise, including:

(1) A profit-seeking enterprise appoints the general manager or its equivalent or superior of another profit-seeking enterprise.

(2) A profit-seeking enterprise that is not a financial institution lends money or provides guarantees to another profit-seeking enterprise to an amount representing 1/3 or more of its total assets.

(3) A profit-seeking enterprise cannot commence its production or business activities without another profit-seeking enterprise’s provision of patents, trademarks, copyrights, secret formulas, proprietary technology, or any franchises, in which the sales of such production and business activities account for 50% or more of the total sales of the former profit-seeking enterprise in the same year.

(4) The price and conditions of a profit-seeking enterprise’s purchase of raw materials, components, and merchandise are controlled by another profit-seeking enterprise; and the purchase of such raw materials, components and merchandise accounts for 50% or more of the total purchase of raw materials, components and merchandise of the former profit-seeking enterprise in the same year.

(5) The sales of products of a profit-seeking enterprise are controlled by another profit-seeking enterprise, and the sales of such products account for 50% or more of the total sales of the former profit-seeking enterprise.

8. A profit-seeking enterprise and another one have entered into a joint venture agreement or an agreement to conduct business jointly.

9. Other circumstances whereby a profit-seeking enterprise has control or major influence over the personnel, finance, business operation or management decisions of another profit-seeking enterprise.

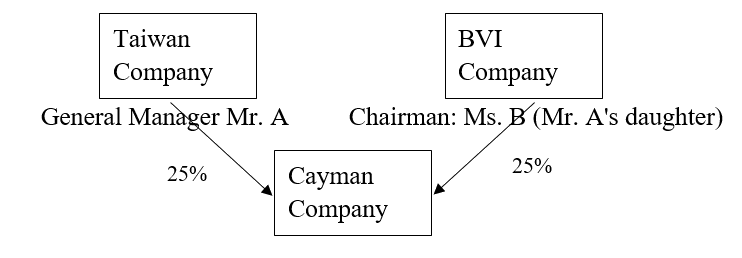

Here we give an example. Mr. A is the general manager of a Taiwan company, while his daughter is the chairman of a BVI company, and the two companies respectively owns 25% of the shareholdings of the Cayman company:

As the Taiwan company and the BVI company respectively owns only 25% of the shareholdings of the Cayman company, it seems that the Cayman company is not the Taiwan company's CFC. However, as Mr. A's daughter is the chairman of the BVI company, the BVI company would be deemed as an "affiliated enterprise" of the Taiwan company. Therefore the Tawian company, together with its affiliated enterprise, holds 50% of the Cayman company, and so the Cayman company would be deemed as the Taiwan company's CFC.

“Related parties other than the affiliated enterprises” shall refer to a domestic or foreign individual, or an educational, cultural, public welfare, or charity organization or group that has any of the following relationships with the profit-seeking enterprise:

- A foundation receives a donation from the profit-seeking enterprise in the amount representing 1/3 or more of the total funds in its balance sheet of such foundation.

- The aggregate number of directors represented by a profit-seeking enterprise and its directors, supervisors, general manager, or its equivalent or superior, or the spouse or blood relations within the second degree of whom reach one half or more of the total number of directors of the foundation.

- A profit-seeking enterprise’s directors, supervisors, general manager or its equivalent or superior, vice general managers, assistant general managers and department heads under the direct supervision of the general manager.

- The spouses of a profit-seeking enterprise’s directors, supervisors, general manager, or its equivalent or superior.

- The relatives within the second degree of a profit-seeking enterprise’s chairperson of the board, or general manager or its equivalent and superior.

- Any person who has control or major influence over the personnel, finance, business operations, or management decisions of a profit-seeking enterprise.

As explained above, when determining whether another profit-seeking enterprise is an affiliated enterprise of a profit-seeking enterprise, it is necessary to examine not only direct and indirect shareholdings (Subparagraphs 1 and 3, Paragraph 2) but also whether there is common control (Subparagraph 2, Paragraph 2), whether the members of the board of directors are the same and how they are designated (Subparagraphs 4 and 5, Paragraph 2), whether the management is the same or has relativeness (Subparagraph 6, Paragraph 2), and whether there is control over personnel, finance or business operations Subparagraphs 7 and 8, Paragraph 2). Subparagraph 9, Paragraph 2 stipulates general provisions to prevent a profit-making enterprise from improperly taking advantage of the loopholes of the criteria specified in the Article.

With respect to related parties other than the affiliated enterprises, if the party is a foundation, it is necessary to pay attention to the source of the donation fund (Subparagraph 1, Paragraph 3) and the composition of the board of directors (Subparagraph 2, Paragraph 3). The management of a profit-seeking enterprise and the spouses and relatives within the second degree of such management are also deemed related parties (Subparagraphs 3, 4 and 5, Paragraph 3). Subparagraph 6, Paragraph 3 also stipulates general provisions to prevent the profit-making enterprise from improperly taking advantage of the loopholes of the criteria specified in the relevant laws and regulations.

Some multinational groups in Taiwan have a complex organizational structure and cross-ownership often exists among the group, making it difficult to determine the related parties. Although the organizational structure of small and medium enterprises is generally less complex than that of multinational groups, common control and the same board of directors issues often exist as well. Therefore, it is recommended that professional assistance be sought in handling CFC filings to avoid being penalized by the competent authorities for declaration errors or failure to declare on time. Lee and Li’s tax team comprises attorneys and CPAs licensed in Taiwan and several other jurisdictions and keeps up with the most advanced development in both domestic taxation and international taxation. Our tax team closely cooperates with L&L, Leaven & Co., CPAs and has an in-depth understanding on the taxation practice of the government authorities. If you have any questions about the Taiwan CFC Rules, please feel free to contact our tax team.