Newsletter

The Determination of Related Parties of the Individuals under the CFC Rules

The Taiwan Individual CFC regime will come into effect on January 1, 2023. A foreign profit-seeking enterprise that meets the specific requirements will be deemed as an individual's Controlled Foreign Corporation (CFC). When the CFC receives dividends from its investment, even if the CFC does not further distribute such dividends to the Taiwan individual shareholder, such dividends may still be required to be included in the Taiwan individual shareholder's basic income in calculating the AMT payable. Generally speaking, a foreign profit-seeking enterprise that meets the following requirements would be deemed as a CFC: (1) the foreign profit-seeking enterprise is established in low-tax jurisdictions; (2) a Taiwanese individual and his or her related parties directly or indirectly hold up to 50% of shares in the foreign profit-seeking enterprise, or have a significant influence on such foreign profit-seeking enterprise; (3) the foreign profit-seeking enterprise does not engage in substantial operating activities; and (4) the foreign profit-seeking enterprise has a net income exceeding NTD 7 million in a fiscal year.

As explained above, as long as a Taiwanese individual, together with his or her related parties, directly or indirectly hold up to 50% of shares in the foreign profit-seeking enterprise, such foreign profit-seeking enterprise may be deemed as a CFC. Therefore, the definition and the recognition of the "related parties" is very important. In this regard, Article 3 of the "Regulations Governing Application of Income Calculation from Controlled Foreign Company for Individual" (the "Individual CFC Regulations") expressly stipulates that "related parties" include the "affiliated enterprises" and the "related parties other than the affiliated enterprises". Paragraphs 2 and 3 of Article 3 of the Individual CFC Regulations stipulate, respectively, the criteria of "affiliated enterprises" and "related parties other than the affiliated enterprises" as follows:

"Affiliated enterprises" shall refer to where there are any of the following situations between an individual and a domestic or foreign profit-seeking enterprise:

1. An individual directly or indirectly holds 20% or more of the total outstanding voting shares or capital stock in a profit-seeking enterprise.

2. An individual holds the highest percentage of the total outstanding voting shares or capital stock in a profit-seeking enterprise and such percentage reaches 10% or more.

3. The aggregate number of directors appointed by one or more profit-seeking enterprise(s) in which an individual directly or indirectly holds over 50% of the total outstanding voting shares or capital stock in another profit-seeking enterprise reaches one half or more of the total number of directors of the latter profit-seeking enterprise.

4. An individual, his or her spouse or relatives within the second degree of kinship being the chairman, general manager, or the equivalent or superior of the profit-seeking enterprise.

5. Other circumstances whereby an individual has control or major influence over the personnel, finance, business operation or management decisions of a profit-seeking enterprise.

"Related parties other than the affiliated enterprises" shall refer to a domestic or foreign individual, or an educational, cultural, public welfare, or charity organization or group that has any of the following relations with the individual:

1. Spouse and relatives within the second degree of kinship.

2. The relatives or family members reported on the same annual individual income tax return filed by the individual.

3. The trustee or the beneficiary who is not the settlor himself/herself of the trust deed created by the individual.

4. A foundation receives a donation from the individual in the amount representing 1/3 or more of the total funds in its balance sheet of such foundation.

5. The foundation in which the aggregate number of directors represented by the individual, his or her spouse, or relatives within the second degree of kinship reaches one half or more of the total number of directors of the foundation.

6. The directors, supervisors, general manager or its equivalent or superior, vice general managers, assistant general managers, and department heads under the direct supervision of the general manager of the affiliated enterprises provided in paragraph 2 of Article 3 of the Individual CFC Regulations.

7. The spouses of the directors, supervisors, general manager, or its equivalent or superior of the affiliated enterprises provided in paragraph 2 of Article 3 of the Individual CFC Regulations.

8. The relatives within the second degree of kinship of the board, or general manager or its equivalent and superior of the affiliated enterprises provided in paragraph 2 of Article 3 of the Individual CFC Regulations.

9. The partner and his or her spouse of a partnership to which the individual or his or her spouse is a partner.

10.Other circumstances whereby an individual has substantive control over the finance, economic, or investment decisions of another individual or an educational, cultural, public welfare, or charity organization or group.

From the above rules, we can know that when determining whether an profit-seeking enterprise is an affiliated enterprise of an individual, it is necessary to examine not only the direct and indirect shareholdings (Subparagraphs 1, Paragraph 2) but also the relative percentage of shareholding in the profit-seeking enterprise (Subparagraphs 2, Paragraph 2), how the board of directors are designated (Subparagraphs 3, Paragraph 2), whether the individual and his or her relatives is the management of the profit-seeking enterprise (Subparagraphs 4, Paragraph 2). Subparagraph 5, Paragraph 2 stipulates general provisions to prevent an individual from improperly taking advantage of the loopholes of the criteria specified in relevant laws and regulations.

With respect to related parties other than the affiliated enterprises, it is necessary to pay attention to the spouses and relatives within the second degree (i.e., brothers and sisters) and the relatives reported on the same annual individual income tax return (Subparagraphs 1 and 2, Paragraph 3). In the event of trust, the trustee and the beneficiary should be paid attention to, in connection with the recognition of related parties under the Individual CFC Regulations (Subparagraph 3, Paragraph 3). In the event of foundation, it is necessary to pay attention to the source of the donation fund (Subparagraph 4, Paragraph 3) and the composition of the board of directors (Subparagraph 5, Paragraph 3). The management of an affiliated enterprises and the spouses and relatives within the second degree of the management of an affiliated enterprise are also deemed related parties (Subparagraphs 6, 7 and 8, Paragraph 3). Subparagraph 10, Paragraph 3 also stipulates general provisions to prevent the individual from improperly taking advantage of the loopholes of the criteria specified in relevant laws and regulations.

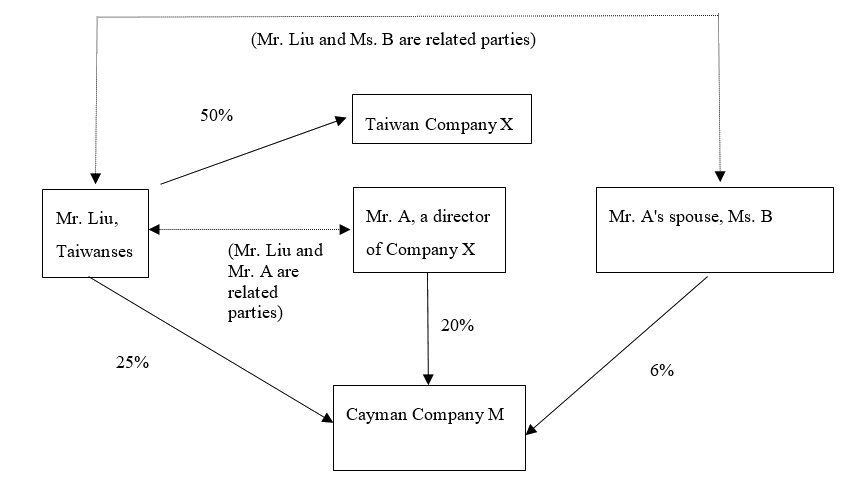

Here we give an example. Assume Mr. Liu owns 25% of Cayman Company M, and owns 50% of Taiwan Company X. Mr. A, a director of Company X, and his spouse, Ms. B, hold 20% and 6% of the shares in Cayman Company M, respectively. The issue here is whether Company M would be deemed as Mr. Liu's CFC?

First, as Mr. Liu holds more than 20% of the shares in Cayman Company X, Cayman Company X is Mr. Liu's related enterprise, pursuant to Subparagraphs 1, Paragraph 2 of Article 3 of the Individual CFC Regulations. Second, as Mr. A is the director of Taiwan Company X, Mr. A is Mr. Liu's related party, pursuant to Subparagraphs 6, Paragraph 3 of Article 3 of the Individual CFC Regulations. As such, Mr. A's shareholding in Cayman Company M shall be included in the calculations when determining whether Mr. Liu holds up to 50% or more of Cayman Company M. Furthermore, as Ms. B is Mr. A's spouse, Ms. B is also Mr. Liu's related party, pursuant to Subparagraphs 7, Paragraph 3 of Article 3 of the Individual CFC Regulations. As such, Ms. B's shareholding in Cayman Company M shall also be included in calculations when determining whether Mr. Liu holds up to 50% or more of Company M.

Based on the above, Mr. Liu's shareholding in Cayman Company M = 25% (direct holding) + (20% + 6%) (indirect holding) = 51%. Therefore, if the other requirements are met (e.g., Cayman Company M does not engage in substantial operating activities), Cayman Company M would be deemed Mr. Liu's CFC.

As explained above, even if an individual's direct shareholding in a foreign enterprise is less than 50%, the CFC regime may still be applicable. For the sake of prudence, it is advisable to examine among each of the shareholders of the foreign enterprise to see whether the shareholders are related parties. Our tax team closely cooperates with L&L, Leaven & Co., CPAs and has an in-depth understanding on the taxation practice of the government authorities. If you have any questions about the Taiwan CFC Rules, please feel free to contact our tax team.